Manual cash application is the hidden bottleneck of the modern finance department. It quietly traps cash in unapplied buckets, slows credit releases, and forces your team into spreadsheet triage when they should be driving decisions. With the global market for cash application automation software projected to reach $6.43 billion by 2033, enterprises are rapidly moving away from error-prone workarounds toward AI-driven reconciliation.

Recent breakthroughs in agentic AI and semantic matching have also raised the bar on what “good” looks like. In many deployments, straight-through processing (STP) moves from “we match some of it automatically” to “we match almost all of it automatically,” with exceptions routed to the right owner and resolved fast.

This article breaks down how automation transforms the order-to-cash cycle, which software providers lead the category, and how to select a tool that fits your ERP, bank files, and real-world remittance chaos.

What is Cash Application Automation Software?

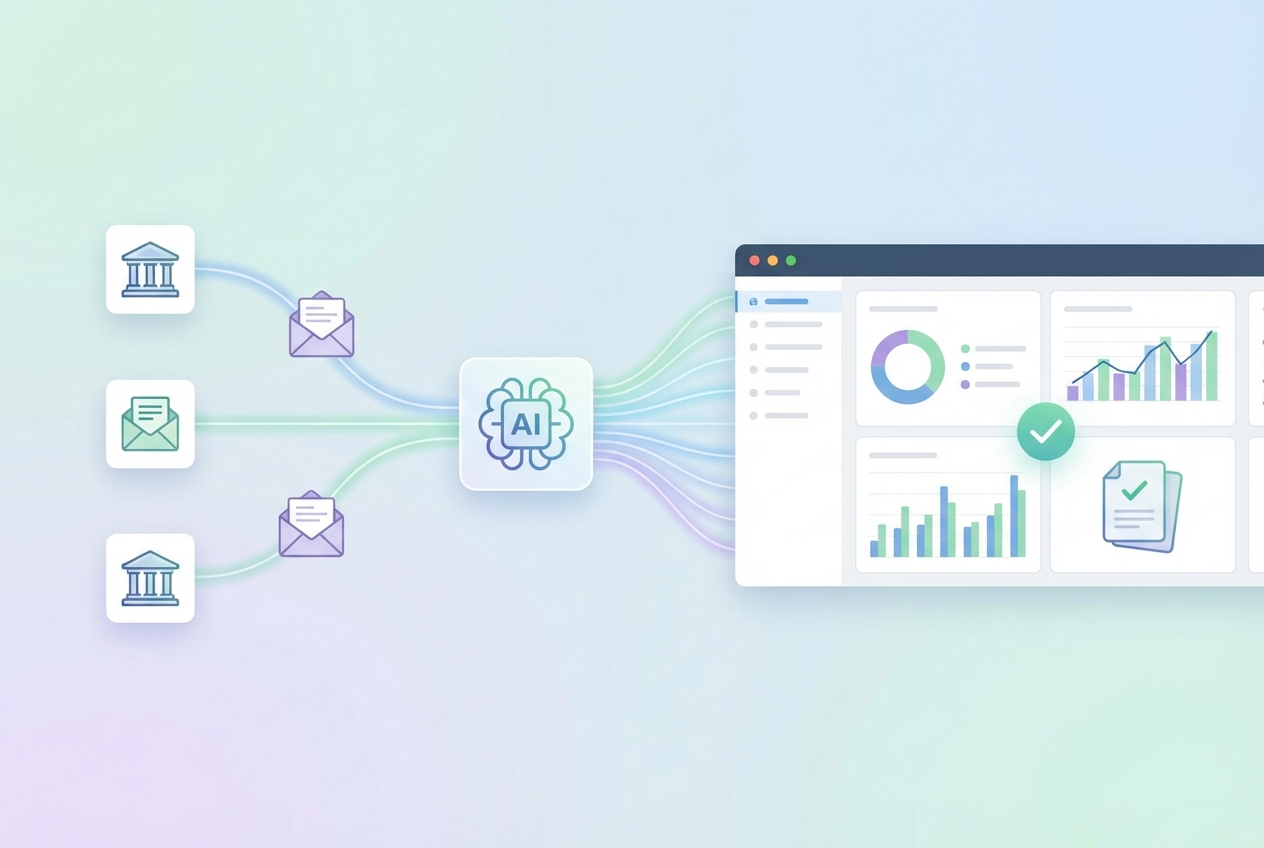

Cash application automation software is a specialized finance tool that matches incoming payments to open invoices and posts the results into your accounting system with minimal human effort. It typically uses a mix of AI (pattern recognition), machine learning (learning from your history), and RPA (robotic process automation) to move data between systems.

This is not the same as “a few rules in your ERP.” Modern automation tools interpret unstructured data like PDF remittances, email text, portal exports, and messy lockbox lines. Then they connect the dots back to invoices.

Gartner groups these capabilities under invoice-to-cash (I2C) applications. These are cloud tools that help finance teams automatically apply payments, manage deductions and disputes, and reduce process cost while improving cash visibility (Gartner market overview).

In practical terms, cash application automation functions as an intelligent layer between your bank and your accounting system:

-

Extract: Pull remittance details from email, PDFs, portals, EDI, and lockbox files using OCR and data parsing.

-

Match: Reconcile payments to invoices using rules plus probabilistic matching (useful when data is incomplete).

-

Post: Write results into your ERP so open AR, customer balances, and credit availability update immediately.

-

Route exceptions: Send short pays, deductions, and unidentified cash to the right person with context attached.

Unlike traditional rule-based systems that fail when data is unstructured, modern workflow automation software can interpret varied formats and keep your process moving without constant babysitting.

By removing delays in posting cash, companies also improve downstream decisions. Credit limits update sooner. Collections sees the truth sooner. Your team stops arguing with yesterday’s spreadsheet and starts operating from current data. That is a direct lever to automate business processes to increase revenue, especially in businesses where shipping, renewals, or usage-based billing depends on clean AR.

Key Benefits of Automating Your Cash Application Process

Transitioning to an automated model provides more than speed. It changes the cost structure of your accounts receivable function and the reliability of your cash picture. One of the most visible process automation benefits is a sharp reduction in manual work that scales linearly with volume.

-

95% reduction in manual work (in well-tuned environments): Best-in-class teams often automate the majority of matches and spend human time only on true exceptions. The Association for Financial Professionals highlights that poor automation wastes resources across the company and that ERPs typically achieve lower matching rates than dedicated cash application solutions.

-

Lower DSO and improved cash flow: Faster posting means fewer customers stuck on hold for credit releases and fewer “phantom delinquencies” caused by unapplied cash. Over time, this pushes DSO down by reducing friction, disputes, and internal delays. Deloitte frames this as freeing “trapped cash” through working capital improvements that can fund growth or reduce debt.

-

Reduced lockbox and keying fees: When remittances are extracted and matched automatically, you rely less on manual bank keying services. Even if you keep lockbox deposits, you can often reduce paid “data entry” add-ons and internal rework.

-

Higher accuracy and cleaner close: Fewer manual touches means fewer misapplied payments, fewer suspense accounts, and less month-end cleanup. That translates into a faster close and better forecasting confidence.

Core Features to Look for in Cash Application Automation Software

Not all “automation” is equal. Many tools can auto-apply clean checks with perfect invoice numbers. The real value shows up when remittances are incomplete, delayed, or split across channels.

AI-Powered Remittance Extraction

Cash application succeeds or fails at intake. You need usable remittance data in the system before matching can work at scale.

Legacy tools struggle with decoupled remittances, where the wire arrives today and the remittance advice arrives later through email or a portal export. Look for software that can:

-

Monitor multiple sources: Email inboxes, SFTP folders, portals, EDI feeds, and lockbox images.

-

Handle unstructured formats: PDFs, screenshots, email bodies, and inconsistent spreadsheets.

-

Learn customer patterns: Common deduction reasons, typical short-pay behaviors, and recurring payment references.

If you want to go further, this is also where modern conversational AI and natural language processing (NLP) becomes practical. “NLP” is simply software that can read messy human language and still extract meaning, like invoice numbers buried in an email thread.

Seamless ERP Integration

Cash application is only valuable when it updates the system your business runs on. Your automation tool should support bi-directional sync with your ERP. That includes SAP, Oracle, NetSuite, and Microsoft Dynamics.

At a minimum, you want:

-

Real-time (or near real-time) posting: Applied cash should update open AR quickly, not in nightly batches.

-

Master data alignment: Customers, invoices, payment terms, and deductions should stay consistent across systems.

-

Auditability: A clear trail from source document to match decision to ERP posting.

This matters beyond finance. When cash is posted promptly, it affects order holds, renewals, and even supply chain automation where inventory and fulfillment depend on credit and payment status.

Intelligent Exception Management

Automating the easy 70% to 80% is table stakes. Your ROI depends on what happens with the rest.

Strong exception management typically includes:

-

Prioritized queues: Work exceptions by dollar value, aging, or customer importance.

-

Collaboration tools: Notes, attachments, and clear handoffs between AR, collections, and sales.

-

Reason codes and workflows: Short pays, discounts, taxes, bank fees, and deductions should follow consistent paths.

-

Customer-facing options (optional): A portal can help customers submit remittances and resolve disputes without email ping-pong.

Leading Cash Application Automation Software Solutions

Several players dominate the landscape. Each is strong in different environments, so the best choice depends on volume, complexity, ERP, and how messy your remittance inputs really are.

Quick comparison

| Vendor | Best for | Strengths | Watch-outs |

|---|---|---|---|

| HighRadius | Global enterprises with complex deductions | Strong AI matching, deep I2C suite, deduction workflows | Can feel heavy for smaller teams; implementation rigor matters |

| Versapay | Mid-market teams that want customer collaboration | Customer portal focus, collaborative AR workflows | Portal adoption depends on your customer base and enablement |

| Esker | Companies automating broader order-to-cash | Strong document lifecycle tools (orders, invoices, AR) | Broader suite can mean broader change management |

| Billtrust | B2B firms with fragmented payment channels | Payments + AR automation, strong remittance digitization | Best value when you leverage more of its platform |

Notes on each provider

- HighRadius: Often chosen by larger organizations that need to handle large volumes, complex deductions, and multi-entity matching. If your biggest pain is “exceptions everywhere,” its workflows can be a strong fit.

- Versapay: Known for a collaborative AR experience. If your customers frequently cause exceptions because remittances arrive late or disputes drag on, a portal-driven approach can reduce cycle time.

- Esker: A good option when your goal is broader order-to-cash automation, not just cash posting. It can make sense if you want one vendor across invoicing, collections, and cash application.

- Billtrust: Often shines in B2B environments with many payment rails and inconsistent remittance sources. It is built for the reality that customers do not all pay the same way.

Implementation Strategy: From Setup to ROI

Most implementations follow a predictable path: connect sources, train matching, configure exceptions, then measure outcomes.

Most implementations follow a predictable path: connect sources, train matching, configure exceptions, then measure outcomes.

Cash application automation does not need to be a multi-year project. The fastest wins come from narrowing scope, getting data flowing, and tuning exceptions with your real history.

A practical rollout plan looks like this:

-

Data aggregation (week 1 to 2): Connect bank feeds, lockbox files, and remittance channels (email, SFTP, portals). Get invoice and customer master data flowing from your ERP.

-

Model training and matching logic (week 2 to 4): Feed historical cash application decisions so the system learns what “right” looks like for your customers. This is where match rates jump, especially for repeat payers with inconsistent references.

-

Workflow configuration (week 3 to 6): Define how exceptions move through your team. Set rules for common scenarios like small-balance write-offs and early pay discounts. Cover tax mismatches and recurring deductions too.

-

Pilot, then expand (week 6+): Start with one entity, one region, or one bank. Stabilize. Then scale.

Where many teams get stuck (and how to avoid it)

-

Over-scoping integrations: Start with the minimum viable integrations that unlock value. Add secondary systems after you prove match rates and exception speed.

-

Ignoring remittance behavior: Your customers drive complexity. Segment them early (top 20 by volume, long-tail, known deduction-heavy accounts) and tune by segment.

-

Treating exceptions as “manual forever”: Exceptions are not a junk drawer. They are patterns waiting to be automated with the right workflows.

When you need a custom layer

Off-the-shelf platforms cover most common workflows. But some businesses still hit edge cases: unique customer hierarchies, unusual billing references, multi-entity settlements, or proprietary portals.

This is where a build-plus-buy approach can be powerful. QuantumByte can help you prototype a lightweight cash application companion app in days, not months. You can use natural language to define what you need, then connect it to your ERP or automation platform via APIs. For example:

-

Remittance intake portal: A simple place for specific customers to upload remittances in the format you prefer, so your team stops hunting through inboxes.

-

Email-to-remittance classifier: A workflow that labels and normalizes attachments before matching, which boosts hit rates when customers send inconsistent PDFs and spreadsheets.

-

Deduction routing workflow: A tailored approval path that assigns ownership, captures reason codes, and prevents “stuck” deductions from aging into write-offs.

If you want to explore what that looks like without committing to a full build cycle, you can map your workflow and start a prototype with QuantumByte.

Optimizing Your Finance Tech Stack

Cash application automation is no longer a luxury reserved for the Fortune 500. It is quickly becoming a baseline requirement for any company that wants to scale without ballooning headcount.

To get the most out of it, treat cash application as part of a connected stack, not a standalone tool:

-

Bank connectivity: Cleaner, more consistent bank data reduces downstream exceptions and speeds matching.

-

ERP discipline: Strong customer master data, invoice structure, and reason codes amplify any automation engine you choose.

-

Collections alignment: When applied cash updates fast, collectors chase the right accounts, not ghosts created by unapplied cash.

-

Dispute and deduction workflows: The sooner you classify and route a deduction, the faster you recover cash or close the loop.

If you are a smaller team, you may not need a “full suite” platform on day one. You may need a sharp, narrow solution plus a small custom layer that matches how you sell, bill, and get paid.

That is another area where QuantumByte fits naturally. When your vendor tool does 80% well but the last 20% is “your business,” a custom workflow can remove the friction that keeps your team in manual mode. The goal is simple: fewer touches, faster posting, and clear ownership for the exceptions that remain.

Turning cash posting into a growth lever

Cash application is not glamorous. But it controls how quickly your business can recognize revenue, release credit, forecast cash, and close the books with confidence.

In this guide, you saw:

-

What it is: How cash application automation software extracts remittances, matches payments, and posts results back to your ERP.

-

Why it matters: The operational wins that show up in DSO, labor load, working capital, and close quality.

-

What to demand: The non-negotiable capabilities, including extraction, ERP integration, and exception workflows.

-

Who to evaluate: Leading tools to shortlist for 2026 based on your volume, complexity, and customer payment behavior.

-

How to implement: A rollout path that gets you to ROI without over-scoping integrations or ignoring exception patterns.

If you take one step this week, make it this: document your remittance sources and top exception types. That single exercise will tell you which platform fits, and whether you need a custom layer to reach true straight-through processing.

Frequently Asked Questions

What is cash application automation software?

It is a technology that uses AI and RPA to automatically match customer payments to their invoices and post the results to an ERP system. It reduces manual data entry and improves reconciliation accuracy.

How does AI improve the cash application process?

AI improves cash application by recognizing patterns in messy remittance data. It learns how specific customers pay, even when invoice numbers are missing or formats change, which increases automatic match rates over time.

Can cash application software integrate with my ERP like SAP or NetSuite?

Yes. Leading cash application automation tools integrate with major ERPs through APIs and connectors, allowing payments to be posted and reflected in open AR with minimal delay.

What is a good automatic match rate for cash application?

Rule-based approaches often plateau because real remittances are inconsistent. A strong AI-driven program should aim for 90%+ straight-through processing once the system is trained and exception workflows are tuned.

How long does it take to see ROI from cash application automation?

Many organizations see ROI within a few months, driven by reduced manual effort, fewer bank-related processing costs, and improved working capital from faster, cleaner posting of cash.